For the love of money is a root of all sorts of evil, and some by longing for it have wandered away from the faith and pierced themselves with many griefs. ~I Timothy 6:10

Again, the devil took Him to a very high mountain and showed Him all the kingdoms of the world and their glory; and he said to Him, “All these things I will give You, if You fall down and worship me.” Then Jesus said to him, “Go, Satan! For it is written, ‘YOU SHALL WORSHIP THE L-RD1 YOUR G-D, AND SERVE HIM ONLY.’” ~Matthew 4:8-10

If I were to ask you, “Who is America’s most dangerous enemy?” how would you answer that?

Let me give you a little information before you respond:

Did you know that you are more likely to die by bee sting, lightning strike or a police shooting than by an Islamic terrorist?

…if terrorists hijacked and crashed one of America’s 18,000 commercial flights per week…your chance of being on the crashed plane would [still only] be one in 135,000. ~ Don’t Be Terrorized, Reason.com

Having a Central Bank to regulate American monetary policy has been an issue since this country’s inception. But we’ve come a long way from multiple disassociated colonies all having different currencies and some of those not even backed by anything negotiable such as a precious metal (gold, etc.).

Anchoring your currency to a precious metal would seem historically prudent but it proves to be an inconvenient nuisance to any organization printing the money.

Even hard-Left Machine apologists like Paul Krugman have to curtsy now and again to acknowledging how dangerous the power of unfettered currency manipulation is (but certainly only a danger in other countries);

The current world monetary system assigns no special role to gold; indeed, the Federal Reserve is not obliged to tie the dollar to anything. It can print as much or as little money as it deems appropriate. There are powerful advantages to such an unconstrained system…

While a freely floating national money has advantages, however, it also has risks. For one thing, it can create uncertainties for international traders and investors. Over the past five years, the dollar has been worth as much as 120 yen and as little as 80. The costs of this volatility are hard to measure (partly because sophisticated financial markets allow businesses to hedge much of that risk), but they must be significant. Furthermore, a system that leaves monetary managers free to do good also leaves them free to be irresponsible—and, in some countries, they have been quick to take the opportunity. That is why countries with a history of runaway inflation, like Argentina, often come to the conclusion that monetary independence is a poisoned chalice. (Argentine law now requires that one peso be worth exactly one U.S. dollar, and that every peso in circulation be backed by a dollar in reserves.) ~ The Gold Bug Variations, Paul Krugman

Certainly, the ability to regulate the finances of an entire country (today, arguably the world’s sole superpower) speaks of power and influence beyond imagination. Such power breathes lust and corruption to attain it and, I’m afraid, the reality will not disappoint you.

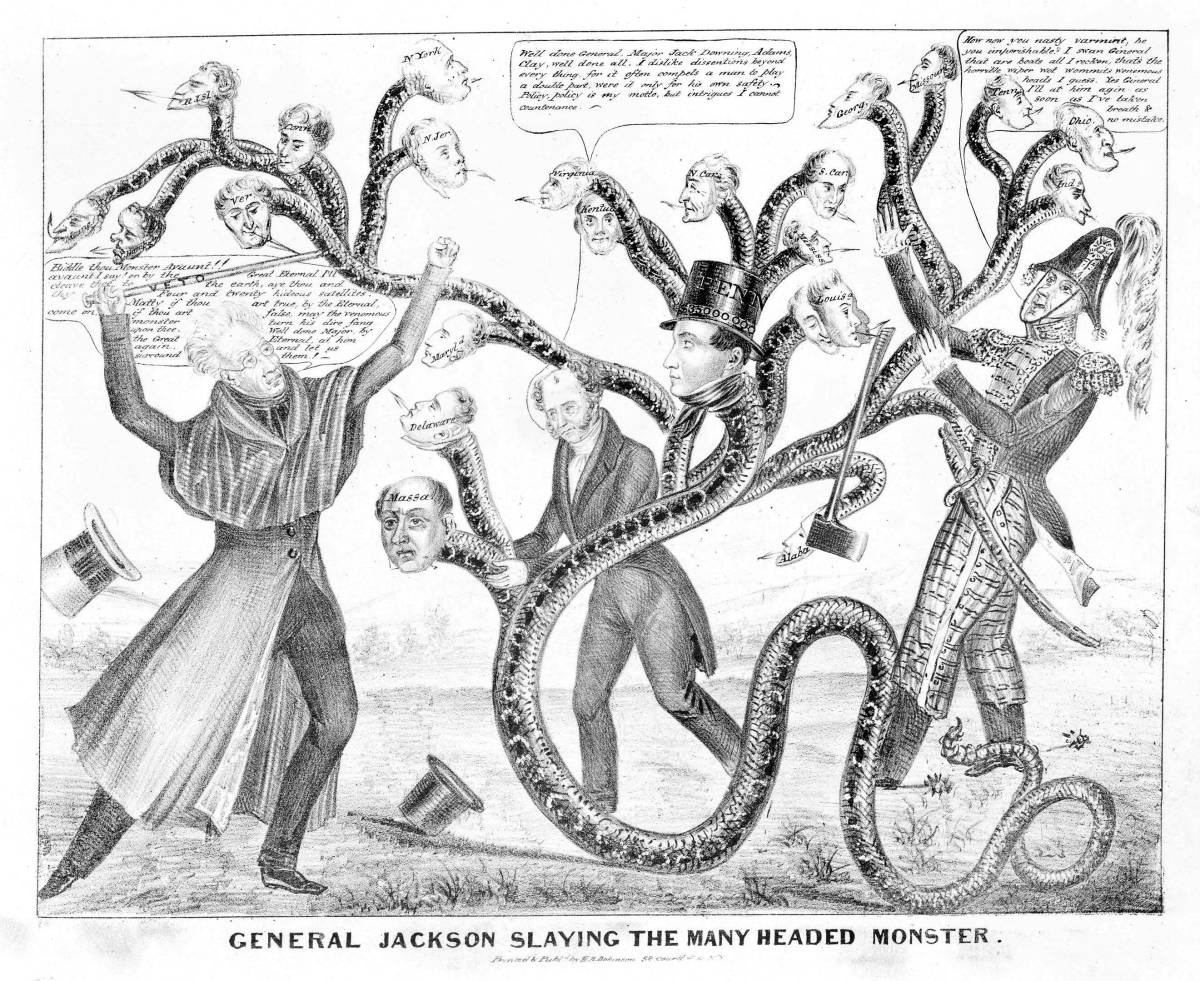

The battle over whether a central banking system is necessary to the State had gone on repeatedly for our first hundred years. Of course standardizing currency and providing market stability were very enticing selling points…until any president ran afoul of being at odds with banking policy and then felt the power of that financial manipulation.

Andrew Jackson made destruction of the Central Bank his life’s work and, although his battle with bank president Nicholas “I Will Pull The Country Down But The Bank Will Not Go Down” Biddle nearly bankrupted him physically, he is credited with being the only president to entirely pay off the national debt.

Andrew Jackson was the only President in American History to pay off the national debt and leave office with the country in the black. ~ “Did You Know?”, The Hermitage, Home of President Andrew Jackson

He is also the first president in American history to have an attempt made on his life.

On the 8th of January, 1835, President Andrew Jackson declared the debt owed by the United States government PAID IN FULL.

A few weeks later, an unemployed housepainter from England pointed first one pistol and then a second at the heart of President Jackson only to have them both miraculously misfire.

Connected?

For starters, it is oddly “coincidental” that one of the wealthiest banking families in all of human history—the Rothschilds—were very busy in England at the time, financing the Napoleonic Wars and capitalizing handily from them. The House of Rothschild would certainly have a vested interest in seeing American finances come under control of a centralized bank.

But several accounts have Lawrence, himself, drawing the connection for onlookers:

Lawrence told doctors later his reasons for the shooting. He blamed Jackson for the loss of his job. He claimed that with the President dead, “money would be more plenty” (a reference to Jackson’s struggle with the Bank of the United States) and that he “could not rise until the President fell.” ~ Andrew Jackson, Wikipedia

Famed Federal Reserve watchdog and researcher G. Edward Griffin noted that Lawrence had later boasted to friends that “powerful people in Europe” had vowed to protect him should he be caught.

Indeed, Lawrence was found not guilty by reason of “insanity”.

Sadly, it was a short-lived reprieve and both bank and debt were back in no-time. The “free banking era” (where banking was regulated by each individual state and all paper was backed by specie such as gold) lasted only until the Civil War

With the ease of counterfeiting and another rash of bank closures, the call went out again to create an all-powerful centralized system of government banking. The National Banking Act (also known as the “National Currency Act”) was passed in 1863 but it is interesting to note the narrow Senate vote of 23-21. How could such a “nuts & bolts” necessity have been so controversial? Did Senators see the same risk of massive corruption and abuse of power?

It wasn’t until 1907 that the hydra began to take the form of the dragon it is today.

Thanks to the “Panic of 1907” (where the New York stock exchange fell almost 50%), a rash of nation-wide bankruptcies was exploited by J.P. Morgan and John D. Rockefeller to call for a centralized system with the power to “infuse liquidity” into America’s economy, set interest rates and, in general, control the purse strings of the nation that many were already seeing as eclipsing Great Britain in world influence thanks to her amazing store of productivity and natural resources.

In fact, the “crisis” was so precipitous to the über rich that an accusation has surfaced that it was fabricated for just the occasion:

The panic of 1907 was sparked when J.P. Morgan, considered a financial luminary at the time, posted rumors in the New York Times [that] several bank(s) were insolvent or bankrupt…this caused massive withdrawals, causing the banks to actually go bankrupt as they weren’t before. As a result Mr. Morgan was able to buy up entire bank chains at a discount price, and also provided an excuse to implement a central bank, (the Federal Reserve) promising financial stability and…a panic…like the one of 1907 would never happen again. ~ Answers.com

Certainly, once there was a crisis, previously-held misgivings about the coalescing of power in the hands of the few were quickly disregarded:

Bankers felt the real problem was that the United States was the last major country without a central bank, which might provide stability and emergency credit in times of financial crisis. While segments of the financial community were worried about the power that had accrued to J.P. Morgan and other “financiers”, most were more concerned about the general frailty of a vast, decentralized banking system… ~ History of central banking in the United States, Wikipedia

The man chosen to write the legislation was Senator Nelson Aldrich. He just happened to be the father-in-law of John D. Rockefeller, Jr. (don’t you love how Ruling Elites keep it all in the family?) and he must’ve made an impact on the Rockefeller family because just a year after the “crisis” of 1907, “Nelson Aldrich Rockefeller” was born—future governor of New York and vice president for Gerald Ford. How quaint! These are what I call “Ruling Elites”—a ruling caste driven by money, right in the middle of the country that supposedly did away with such strictly-defined fiefdoms!

Now, interestingly enough, the drafting of this extremely important legislation wasn’t done in any conventional way. Aldrich sent his private railroad car (the Lear Jet of the time, isn’t that nice?) to pick up five people—none of whom were given permission to acknowledge the other or even use their real names:

The 1910 “duck hunt” on Jekyll Island included Senator Nelson Aldrich, his personal secretary Arthur Shelton, former Harvard University professor of economics Dr. A. Piatt Andrew, J.P. Morgan & Co. partner Henry P. Davison, National City Bank president Frank A. Vanderlip and Kuhn, Loeb, and Co. partner Paul M. Warburg. From the start the group proceeded covertly. They began by shunning the use of their last names and met quietly at Aldrich’s private railway car in New Jersey. In 1916, B. C. Forbes discussed the Jekyll conference in his book Men Who Are Making America and illuminates, “To this day these financiers are Frank and Harry and Paul [and Piatt] to one another and the late Senator remained ‘Nelson’ to them until his death. Later [following the Jekyll conference] Benjamin Strong, Jr., was called into frequent consultation and he joined the ‘First-Name Club’ as ‘Ben.’” ~ The Jekyll Island Duck Hunt That Created The Federal Reserve, By Tyler E. Bagwell

What’s a “Jekyll Island” you ask (besides one of the most aptly-named locations in human history)? —Why, it’s a secretive, secluded resort for the rich & shameless, of course! Where else would you go to author one of the most seminal pieces of legislation in United States history?!

On the 25th of March, 2011, Glenn Beck noted on his now-cancelled Fox TV show that this coterie of “duck hunters” represented 1/4th of the wealth of the entire world. Some have suggested that doing programs of this nature and on this material is what got Glenn cancelled, even though he was (and still is) certainly one of the most popular prognosticators in his class.

During that same program, Glenn itemized the agenda of this meeting and it is an insightful look into all agendas of the Elites:

- Stop the growing competition.

- Obtain the franchise to create money out of nothing and set the interest rate.

- Get control of all bank reserves.

- Shift any losses to the taxpayers.

- Convince Congress that the purpose was to protect the taxpayers.

The amount of direct oversight the American people have on the “Federal” Reserve is nil.

Organization of the Federal Reserve System

The Federal Reserve System has both private and public components, and can make decisions without the permission of Congress or the President of the U.S. The System … derives its authority and purpose from the Federal Reserve Act passed by Congress in 1913. The four main components of the Federal Reserve System are (1) the Board of Governors, (2) the Federal Open Market Committee, (3) the twelve regional Federal Reserve Banks, and (4) the member banks throughout the country.

Federal Reserve Board of Governors

The seven-member Board of Governors is a federal agency. It is charged with the overseeing of the 12 District Reserve Banks and setting national monetary policy. It also supervises and regulates the U.S. banking system in general. Governors are appointed by the President of the United States and confirmed by the Senate for staggered 14-year terms. The Board is required to make an annual report of operations to the Speaker of the U.S. House of Representatives.

The Chairman and Vice Chairman of the Board of Governors are appointed by the President from among the sitting Governors. They both serve a four year term and they can be renominated as many times as the President chooses, until their terms on the Board of Governors expire.

Conspicuously absent in the process is the body within the central government that is the most responsive to the people; the House of Representatives. Elected every two years from within small districts, the House is much more restrained by the people than the Senate (every six years from voters across the entire state) or the Chief Executive (every four years from voters across the entire country, but first filtered through the Electoral College).

Not only are they insulated from the voters, but once appointed by the president, a member of the Board of Governors can not be removed!

Once appointed, governors cannot be removed from office… ~ Board of the Governors of the Federal Reserve System, The Federal Reserve Bank of New York

And a Chairman and Vice Chairman can only be selected from amongst the sitting Governors!

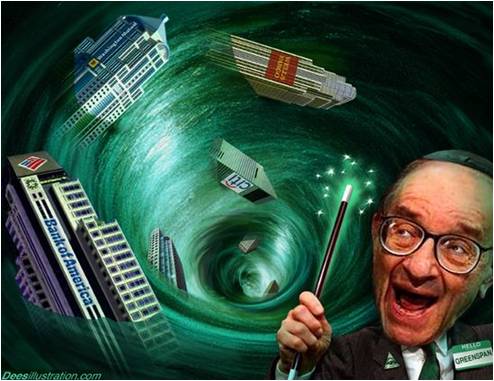

This “autonomy” is so safe for “the Fed” that one former Chairman even bragged about it publicly!

This week, former chairman of the Fed Reserve Alan Greenspan in an interview aired on PBS’ News Hour was asked by Jim Lehrer what should be the proper relationship between a chairman of the Fed and The President of the United States. In a shockingly honest tone Greenspan replied, “Well, first of all, the Federal Reserve is an independent agency, and that means, basically, that there is no other agency of government which can overrule actions that we take. So long as that is in place and there is no evidence that the administration or the Congress or anybody else is requesting that we do things other than what we think is the appropriate thing, then what the relationships are don’t, frankly, matter.” ~ Greenspan Admits Fed Is Not Beholden To Any Government Agency, Prisonplanet.com, 21 September, 2007

Greenspan would know, he was Chairman of the “Federal” Reserve for nearly twenty years. Prior to that he worked as a managing director at the Wall Street investment bank Brown Brothers Harriman.

It is an interesting aside to note that Alan Greenspan’s personal life does wonders for the “conspiracy crowd” who have fits whenever they see evidence of collusion amongst Elites from across various disciplines (especially government, media and corporate/banking/finance—where all the power is);

Greenspan has married twice. His first marriage was to an artist named Joan Mitchell in 1952; the marriage ended in annulment less than a year later. He dated newswoman Barbara Walters in the late 1970s. In 1984, Greenspan began dating journalist Andrea Mitchell. Greenspan at the time was 58; Mitchell is 20 years younger. In 1997, they were married by [radical Leftist and former ACLU lawyer] Supreme Court Justice Ruth Bader Ginsburg. ~ Alan Greenspan, Wikipedia

By the way, also fueling the sense of futility amongst Right-minded American Patriots regarding whether or not they are truly represented by anyone in Congress (least of all “Republicans”), the controversial Ginsberg was approved in her Senate confirmation hearing by an astounding 96 to 3 vote.

By the way, also fueling the sense of futility amongst Right-minded American Patriots regarding whether or not they are truly represented by anyone in Congress (least of all “Republicans”), the controversial Ginsberg was approved in her Senate confirmation hearing by an astounding 96 to 3 vote.

I found it ironic to the point of dark humor to read this in Greenspan’s user-edited Wikipedia bio:

Greenspan came to the Federal Reserve Board from a successful consulting career, holding economic views influenced by [Libertarian laissez-faire heroine] Ayn Rand.

—and later read an article from the Ayn Rand Center calling Greenspan out as a pseudo capitalist and Machiavellian wrecking ball:

…according to Dr. Yaron Brook, executive director of the Ayn Rand Center for Individual Rights, “any belief Greenspan ever had in truly free markets was abandoned long ago. While Greenspan long ago wrote in favor of a truly free market in banking, including the gold standard that such markets always adopt, he then proceeded to work for two decades as leader and chief advocate of the Federal Reserve, which continually inflates the money supply and manipulates interest rates. Advocates of free banking understand that when the government inflates the currency, it artificially increases prices and causes booms in certain sectors of the economy, followed by inevitable busts. But not only did Greenspan lead the inflation behind the dot-com bubble and the real estate boom, he blamed the market for their treacherous collapses. Greenspan should have recognized that what he wrote in 1966 of the boom preceding the 1929 crash applied here: ‘The excess credit which the Fed pumped into the economy spilled over into the stock market—triggering a fantastic speculative boom.’ Instead, he superficially blamed ‘infectious greed.’”

“Should it be any shock that Greenspan now blames the free market for today’s meltdown—rather than the Fed’s policies, which fueled an inflationary housing boom, which rewarded reckless lenders and borrowers from Wall Street to Main Street? Greenspan didn’t mention the word ‘inflation’ once in his testimony.”

“Whatever Greenspan’s economic philosophy is, it is not anything resembling a free market.” ~ Greenspan Has No Free Market Philosophy, Ayn Rand Center, 24 October, 2008

Yet, this portrait perfectly defines, not only the frightening amount of power wielded by this position and this institution, but also how it seems truly “hell-bent” on the destruction of American prosperity.

The so-called “housing bubble” that wrecked tens of thousands of families all across America didn’t bother Greenspan. In fact, he was more interested in keeping the facts of the issue in the rarified air of his elite little clique of financiers.

As top Federal Reserve officials debated whether there was a housing bubble and what to do about it, then-Chairman Alan Greenspan argued that dissent should be kept secret so that the Fed wouldn’t lose control of the debate to people less well-informed than themselves.

“We run the risk, by laying out the pros and cons of a particular argument, of inducing people to join in on the debate, and in this regard it is possible to lose control of a process that only we fully understand,” Greenspan said, according to the transcripts of a March 2004 meeting. ~ Greenspan Wanted Housing-Bubble Dissent Kept Secret, Ryan Grim, The Huffington Post, 03 July 2010

Certainly, when examining Federal Reserve policies previous to the “housing bubble” bursting, one can see why Mr. Greenspan would rather only he discuss such lofty matters.

In a Left-leaning article claiming “not enough” government regulation was the cause (it was actually too much government regulation requiring mortgages be given to low-income minorities who repaid their loans with Democrat votes), we still get a grain of truth;

The commission that investigated the crisis casts a wide net of blame, faulting two administrations, the Federal Reserve and other regulators for permitting a calamitous concoction: shoddy mortgage lending, the excessive packaging and sale of loans to investors and risky bets on securities backed by the loans.

“The greatest tragedy would be to accept the refrain that no one could have seen this coming and thus nothing could have been done,” the panel wrote in the report’s conclusions, which were read by The New York Times. ~ Financial Crisis Was Avoidable, Inquiry Finds, SEWELL CHAN, The New York Times, 25 January, 2011

In front of Alan Greenspan (or more preferably behind him?) in this despicable debacle is the openly homosexual Democrat Congressman from the state of Massachusetts, Barney Frank. After over thirty years as a United States Congressman (re-elected by the good citizens of his district more than fifteen times), Judicial Watch’s third most corrupt politician for 2009 and the man who’s “room-mate” used to run male “courtiers” out of their domicile is finally going to retire; satisfied and well-rested after all the poison he has sewn in that time.

Teaming up with the Federal Reserve Bank of Boston, the two were an unbeatable team of destruction:

The roots of this crisis go back to the Carter administration. That was when government officials, egged on by left-wing activists, began accusing mortgage lenders of racism and “redlining” because urban blacks were being denied mortgages at a higher rate than suburban whites.

The pressure to make more loans to minorities (read: to borrowers with weak credit histories) became relentless. Congress passed the Community Reinvestment Act, empowering regulators to punish banks that failed to “meet the credit needs” of “low-income, minority, and distressed neighborhoods.” Lenders responded by loosening their underwriting standards and making increasingly shoddy loans. The two government-chartered mortgage finance firms, Fannie Mae and Freddie Mac, encouraged this “subprime” lending by authorizing ever more “flexible” criteria by which high-risk borrowers could be qualified for home loans, and then buying up the questionable mortgages that ensued.

All this was justified as a means of increasing homeownership among minorities and the poor. Affirmative-action policies trumped sound business practices. A manual issued by the Federal Reserve Bank of Boston advised mortgage lenders to disregard financial common sense. “Lack of credit history should not be seen as a negative factor,” the Fed’s guidelines instructed. Lenders were directed to accept welfare payments and unemployment benefits as “valid income sources” to qualify for a mortgage. Failure to comply could mean a lawsuit.

As long as housing prices kept rising, the illusion that all this was good public policy could be sustained. But it didn’t take a financial whiz to recognize that a day of reckoning would come. “What does it mean when Boston banks start making many more loans to minorities?” I asked in this space in 1995. “Most likely, that they are knowingly approving risky loans in order to get the feds and the activists off their backs … When the coming wave of foreclosures rolls through the inner city, which of today’s self-congratulating bankers, politicians, and regulators plans to take the credit?” ~ Frank’s Fingerprints Are All Over the Financial Fiasco, Jeff Jacoby, The Boston Globe, 28 September, 2008

Frank has certainly done his best to take care of his banker elite friends.

Bankers Get $4 Trillion Gift From Barney Frank: David Reilly

David Reilly – 29 Dec, 2009 9:00 PM ET

Bloomberg OpinionTo close out 2009, I decided to do something I bet no member of Congress has done — actually read from cover to cover one of the pieces of sweeping legislation bouncing around Capitol Hill.

Hunkering down by the fire, I snuggled up with H.R. 4173, the financial-reform legislation passed earlier this month by the House of Representatives. … The baby of Financial Services Committee Chairman Barney Frank, the House bill is meant to address everything from too-big-to-fail banks to asleep-at-the-switch credit-ratings companies to the protection of consumers from greedy lenders.

The reading was especially painful since this reform sausage is stuffed with more gristle than meat. At least, that is, if you are a taxpayer hoping the bailout train is coming to a halt.

If you’re a banker, the bill is tastier. While banks opposed the legislation, they should cheer for its passage by the full Congress in the New Year: There are huge giveaways insuring the government will again rescue banks and Wall Street if the need arises.

Here are some of the nuggets I gleaned from days spent reading Frank’s handiwork:

* For all its heft, the bill doesn’t once mention the words “too-big-to-fail,” the main issue confronting the financial system. …

* Instead, it supports the biggest banks. It authorizes Federal Reserve banks to provide as much as $4 trillion in emergency funding the next time Wall Street crashes. So much for “no-more-bailouts” talk. That is more than twice what the Fed pumped into markets this time around.

* Oh, hold on, the Federal Reserve and Treasury Secretary can’t authorize these funds unless “there is at least a 99 percent likelihood that all funds and interest will be paid back.” Too bad the same models used to foresee the housing meltdown probably will be used to predict this likelihood as well.

More Bailouts

* The bill also allows the government, in a crisis, to back financial firms’ debts. Bondholders can sleep easy — there are more bailouts to come.

______________________

Fear of servitude makes strange bedfellows and they get no stranger than Libertarian Ron Paul (R, TX) and avowed Socialist Bernie Sanders (D, VT) who pushed adamantly that the Federal Reserve be audited. They were joined by staunch conservative Jim DeMint (R, SC) and Alan Grayson (D, FL) of “the Republicans want you dead” fame. The proposed legislation (H.R. 1207: Federal Reserve Transparency Act of 2009) elicited an interesting response for Chairman Ben Bernake.

In testimony before the House Oversight Committee, Bernake was asked by Representative John Duncan (R, TN), “Do you think it would cause problems for the Fed or for the economy if that legislation was to pass?”

To which Bernake responded, “My concern about the legislation is that if the GAO [Government Accounting Office] is auditing not only the operational aspects of our programs and the details of the programs but is making judgments about our policy decisions, that would effectively be a takeover of monetary policy by the Congress—a repudiation of the independence of the Federal Reserve which would be highly destructive to the stability of the financial system, the dollar and our national economic situation.”

The former Stanford School of Business professor had little to worry about. In spite of having an amazing level of support, there’s always the cockroach who crawls up out of the woodwork to save the day.

In this case, the cockroach’s name was “Mel Watt” (D, NC);

The bill, with 308 co-sponsors, has been stripped of provisions that would remove Fed exemptions from audits of transactions with foreign central banks, monetary policy deliberations, transactions made under the direction of the Federal Open Market Committee and communications between the Board, the reserve banks and staff, Paul said today.

“There’s nothing left, it’s been gutted,” he said in a telephone interview. “…People all over the country want to know what the Fed is up to, and this legislation was supposed to help them do that.”

The Fed, led by Chairman Ben S. Bernanke, has come under greater congressional scrutiny while attempting to end the financial crisis by bailing out financial firms and more than doubling its balance sheet to $2.16 trillion in the past year. The central bank is also buying $1.25 trillion of securities tied to home loans. ~ Federal Reserve Policy Audit Legislation “Gutted”, Paul Says, Bob Ivry, Bloomberg, 30 October, 2009

Perhaps, learning his lesson at long last, Paul became a subversive of his own, sliding it into the aforementioned “Dodd–Frank Wall Street Reform and Consumer Protection Act” (if you ever want to know what a piece of legislation is supposed to do, take the name and inverted it to the polar opposite of what it says)—and inserting an audit clause amongst the 849 pages of insider protectionism and massive crony corruption.

The results were only a partial audit of the Fed but even so, it was enough to make your blood run cold.

As you peel back the layers of the rotten onion, the numbers in secret “loans” to banks all around the world get bigger and bigger and bigger; $8 trillion, $13 trillion, $16 trillion.

The American taxpayer was swindled to the tune of $786 billion for the TARP bailout of banks that were “too big to fail.” But at least we knew about it.

Thanks to language inserted into the Dodd-Frank bill by Ron Paul, a partial and very begrudging audit of the Federal Reserve has revealed that some of Mittens Romneycare’s biggest donors got over $7.7 TRILLION in secret, smoke-filled-room, under-the-table bailouts from the Federal Reserve.

It took three years of Freedom of Information Act requests by Bloomberg to get details of the secret bailouts and the massive swindle of the American people they represented. ~ Federal Reserve’s Secret Bailouts Totaled Nearly $8 Trillion, Kathleen Gee, HillBuzz.org, 02 December, 2011

Perhaps the most amazing aspect of the story is that the emergency loan data ever saw the light of day. It wasn’t an easy process. Bloomberg originally tried to obtain information pertaining to bailouts through a Freedom of Information Act request. When the Federal Reserve and banks fought against fulfilling the request, Bloomberg took the matter all the way to the Supreme Court, which finally denied a financial industry appeal to keep the relevant documents out of the public eye earlier this year. Bloomberg then quietly began sifting through the paperwork. ~ Ron Paul and Company Vindicated on Fed Audit, Joseph Lawler, The American Spectator, 02 December 2011

The Bloomberg article is written in tame fashion, mitigating the astounding outrage in its entirety with caveats like claiming “the loans were all repaid”.

Sure they were. And you can prove it with these ledgers right here (don’t mind the pencil and crayons).

The Federal Reserve and the big banks fought for more than two years to keep details of the largest bailout in U.S. history a secret. Now, the rest of the world can see what it was missing.

The Fed didn’t tell anyone which banks were in trouble so deep they required a combined $1.2 trillion on Dec. 5, 2008, their single neediest day. Bankers didn’t mention that they took tens of billions of dollars in emergency loans at the same time they were assuring investors their firms were healthy. And no one calculated until now that banks reaped an estimated $13 billion of income by taking advantage of the Fed’s below-market rates…

…The amount of money the central bank parceled out was surprising even to Gary H. Stern, president of the Federal Reserve Bank of Minneapolis from 1985 to 2009, who says he “wasn’t aware of the magnitude.” It dwarfed the Treasury Department’s better-known $700 billion Troubled Asset Relief Program, or TARP. Add up guarantees and lending limits, and the Fed had committed $7.77 trillion as of March 2009 to rescuing the financial system, more than half the value of everything produced in the U.S. that year.

“TARP at least had some strings attached,” says Brad Miller, a North Carolina Democrat on the House Financial Services Committee, referring to the program’s executive-pay ceiling. “With the Fed programs, there was nothing.” ~ Secret Fed Loans Gave Banks $13 Billion Undisclosed to Congress, Bob Ivry, Bradley Keoun and Phil Kuntz, Bloomberg Markets Magazine, – 27 November, 2011

TOO BIG TO FAIL

As I said before, Elites love a crisis. When a crisis hits, then you can really do some damage; subvert Constitutional restrictions on your power, steal massive amounts of taxpayer money and throw tyrannical levels of control upon the citizenry and they’ll even ask you to do it!

The problem is, there’s never a good crisis around when you need one … unless you make it.

The Troubled Asset Relief Program was sold to the American people as the necessary response to the crisis of too many people receiving mortgage loans who couldn’t pay them—a crisis created by government regulation and Federal Reserve currency manipulation.

The numbers on the check Congress wrote for the taxpayer to pay were, of course, hidden deep within more insider legislation but rumors had them to be anywhere from $475 to well over $800 billion. President George W. Bush, son of former president George H.W. Bush, sheepishly signed it into reality.

From there, the bankers quickly went to work.

Many of the banks that got federal aid to support increased lending have instead used some of the money to make investments, repay debts or buy other banks, according to a new report from the special inspector general overseeing the government’s financial rescue program.

The report, which will be published Monday, surveyed 360 banks that got money through the end of January and found that 110 had invested at least some of it, 52 had repaid debts and 15 had used funds to buy other banks.

Roughly 80 percent of respondents, or 300 banks, also said at least some of the money had supported new lending. ~ Banks Misused TARP Funds, Says Inspector General, Binyamin Appelbaum, The Washington Post

It’s not the first time this game has been played, but the stakes get higher and higher with each gambit. And it uncovers the dirty little secret about the “free-market capitalism” of “Wall Street”:

—It doesn’t exist.

The effort to save Fannie Mae and Freddie Mac is only the latest in a series of financial maneuvers by the government that stretch back to the rescue of the military contractor Lockheed Aircraft and the Penn Central Railroad under President Richard Nixon, the shoring up of Chrysler in the waning days of the Carter administration and the salvage of the U.S. savings and loan system in the late 1980s. …

Now, with the U.S. government preparing to save Fannie and Freddie only six months after the Federal Reserve Board orchestrated the rescue of Bear Stearns, it appears that the mortgage crisis has forced the government to once again shove ideology aside and get into the bailout business.

“If anybody thought we had a pure free-market financial system, they should think again,” said Robert Bruner, dean of the Darden School of Business at the University of Virginia. ~ Mortgage Crisis Has Washington Putting Aside Free-Market Ideology, Nelson D. Schwartz, The New York Times, 07 September, 2008

The Bear Sterns bailout; just a blip on the radar of mainstream media, sandwiched in between NY governor Elliot Spitzer’s scandal of using public money to visit prostitutes in another state and polar bears listed as threatened by you breathing too much.

The mother of all insider trades was pulled off in 1815, when London financier Nathan Rothschild led British investors to believe that the Duke of Wellington had lost to Napoleon at the Battle of Waterloo. In a matter of hours, British government bond prices plummeted. Rothschild, who had advance information, then swiftly bought up the entire market in government bonds, acquiring a dominant holding in England’s debt for pennies on the pound. Over the course of the nineteenth century, N. M. Rothschild would become the biggest bank in the world, and the five brothers would come to control most of the foreign-loan business of Europe. “Let me issue and control a nation’s money,” Rothschild boasted in 1838, “and I care not who writes its laws.”

In the United States a century later, John Pierpont Morgan again used rumor and innuendo to create a panic that would change the course of history. The panic of 1907 was triggered by rumors that two major banks were about to become insolvent. Later evidence pointed to the House of Morgan as the source of the rumors. The public, believing the rumors, proceeded to make them come true by staging a run on the banks. Morgan then nobly stepped in to avert the panic by importing $100 million in gold from his European sources. The public thus became convinced that the country needed a central banking system to stop future panics, overcoming strong congressional opposition to any bill allowing the nation’s money to be issued by a private central bank controlled by Wall Street; and the Federal Reserve Act was passed in 1913. Morgan created the conditions for the Act’s passage, but it was Paul Warburg who pulled it off. An immigrant from Germany, Warburg was a partner of Kuhn, Loeb, the Rothschilds’ main American banking operation since the Civil War. Elisha Garrison, an agent of Brown Brothers bankers, wrote in his 1931 book Roosevelt, Wilson and the Federal Reserve Law that “Paul Warburg is the man who got the Federal Reserve Act together after the Aldrich Plan aroused such nationwide resentment and opposition. The mastermind of both plans was Baron Alfred Rothschild of London.” Morgan, too, is now widely believed to have been Rothschild’s agent in the United States.

Robert Owens, a co-author of the Federal Reserve Act, later testified before Congress that the banking industry had conspired to create a series of financial panics in order to rouse the people to demand “reforms” that served the interests of the financiers. A century later, JPMorgan Chase & Co. (now one of the two largest banks in the United States) may have pulled this ruse off again, again changing the course of history. “Remember Friday March 14, 2008,” wrote Martin Wolf in The Financial Times; “it was the day the dream of global free-market capitalism died.”

The “rescuer” was not actually JP Morgan but was the Federal Reserve, the “bankers’ bank” set up by J. Pierpont Morgan to backstop bank runs; and the party “rescued” was not Bear Stearns, which wound up being eaten alive. The Federal Reserve (or “Fed”) lent $25 billion to Bear Stearns and another $30 billion to JP Morgan, a total of $55 billion that all found its way into JP Morgan’s coffers. It was a very good deal for JP Morgan and a very bad deal for Bear’s shareholders, who saw their stock drop from a high of $156 to a low of $2 a share. Thirty percent of the company’s stock was held by the employees, and another big chunk was held by the pension funds of teachers and other public servants. The share price was later raised to $10 a share in response to shareholder outrage and threats of lawsuits, but it was still a very “hostile” takeover, one in which the shareholders had no vote. …

The deal was also a very bad one for U.S. taxpayers, who are on the hook for the loan. ~ The Secret Bailout of J. P. Morgan: How Insider Trading Looted Bear Stearns and the American Taxpayer, Ellen Brown, Global Research, 14 May, 2008

Interestingly enough, the endless streams of “Federal Reserve Notes” gushing to Wall Street suddenly dried up when the streams hit Main Street:

Federal Reserve Chairman Ben Bernanke on Friday ruled out a central bank bailout of state and local governments strapped with big municipal debt burdens, saying the Fed had limited legal authority to help and little will to use that authority.

“We have no expectation or intention to get involved in state and local finance,” Mr. Bernanke said in testimony before the Senate Budget Committee. The states, he said later, “should not expect loans from the Fed.” ~ Bernanke Rejects Bailouts: Fed Chief Says State and Local Governments Shouldn’t Expect Federal Loans, Jon Hilsenrath and Neil King Jr., The Wall Street Journal, 08 January, 2011

As an effort to stabilize the economy, lending and home ownership for Americans, TARP was a colossal failure.

As a stealthy attempt on a massive redistribution of wealth from common citizenry to the Elite, it was a spectacular success:

The $700 billion dollar TARP bailout was a massive bait-and-switch. The government said it was doing it to soak up toxic assets, and then switched to saying it was needed to free up lending. It didn’t do that either. Indeed, the Fed doesn’t want the banks to lend.

As I wrote in March 2009, the bailout money is just going to line the pockets of the wealthy, instead of helping to stabilize the economy or even the companies receiving the bailouts:

■ Bailout money is being used to subsidize companies run by horrible business men, allowing the bankers to receive fat bonuses, to redecorate their offices, and to buy gold toilets and prostitutes.

■ A lot of the bailout money is going to the failing companies’ shareholders.

■ Indeed, a leading progressive economist says that the true purpose of the bank rescue plans is “a massive redistribution of wealth to the bank shareholders and their top executives”.

■ The Treasury Department encouraged banks to use the bailout money to buy their competitors, and pushed through an amendment to the tax laws which rewards mergers in the banking industry (this has caused a lot of companies to bite off more than they can chew, destabilizing the acquiring companies).

And as the New York Times notes, “Tens of billions of [bailout] dollars have merely passed through A.I.G. to its derivatives trading partners”. ~ Government Says No to Helping States and Main Street, While Continuing to Throw Trillions at the Giant Banks, Washington’s Blog, 13 January, 2011

But the redistribution of wealth wasn’t just to American banks. Foreign banks sidled up to the American taxpayer trough as well, and ole’ Happy Bernake worked that pump handle as fast as he could.

Foreign Borrowers

It wasn’t just American finance. Almost half of the Fed’s top 30 borrowers, measured by peak balances, were European firms. They included Edinburgh-based Royal Bank of Scotland Plc, which took $84.5 billion, the most of any non-U.S. lender, and Zurich-based UBS AG (UBSN), which got $77.2 billion. Germany’s Hypo Real Estate Holding AG borrowed $28.7 billion, an average of $21 million for each of its 1,366 employees.

The largest borrowers also included Dexia SA (DEXB), Belgium’s biggest bank by assets, and Societe Generale SA, based in Paris, whose bond-insurance prices have surged in the past month as investors speculated that the spreading sovereign debt crisis in Europe might increase their chances of default.

The $1.2 trillion peak on Dec. 5, 2008 — the combined outstanding balance under the seven programs tallied by Bloomberg — was almost three times the size of the U.S. federal budget deficit that year and more than the total earnings of all federally insured banks in the U.S. for the decade through 2010, according to data compiled by Bloomberg. ~ Wall Street Aristocracy Got $1.2 Trillion in Secret Loans, Bradley Keoun and Phil Kuntz, Bloomberg, 22 August, 2011

Of course, if any of the players should have an attack of conscience to the point of being a liability, it’s much more likely that they just end up getting …

— “depressed”.

(Oddly enough, there wasn’t much national coverage on this story.)

Official Cause of Freddie Mac CFO’s Death May Take Weeks

WTOP, Fairfax County, Virginia

Thursday – 23 April, 2009, 2:04pm ETVIENNA, Va. – Medical examiners have completed an autopsy on the acting chief financial officer of Freddie Mac found dead in an apparent suicide, but the final determination of the cause of death could take weeks.

David Kellermann, 41, was found dead in his Vienna home early Wednesday morning. Police say Kellermann’s death was an apparent suicide.

Nancy Bull, the regional administrator for the medical examiner’s office, told the Associated Press on Thursday that the final determination won’t be made until all the lab results are received. Bull says the preliminary findings are consistent with a suicide.

“Stimulus” ordo ab chao

After slowing down the economy to a snail’s pace by bleeding the taxpayer and treasury dry, the Democrat-controlled Congress got a boost: a Democrat president. While George W. Bush played footsie with the brake of fiscal implosion, Barack Hussein Obama kicked it off and then-Speaker of the House Nancy Pelosi stamped on the accelerator.

Slated as a “stimulus” for the economy, it became a perpetual Christmas morning for politicians and their supporters and the American taxpayer (few as actual taxpayers are now) footed the bill.

“Never let a serious crisis go to waste. What I mean by that is it’s an opportunity to do things you couldn’t do before.”

So said White House Chief of Staff Rahm Emanuel in November, and Democrats in Congress are certainly taking his advice to heart. The 647-page, $825 billion House legislation is being sold as an economic “stimulus,” but now that Democrats have finally released the details we understand Rahm’s point much better. This is a political wonder that manages to spend money on just about every pent-up Democratic proposal of the last 40 years.

We’ve looked it over, and even we can’t quite believe it. There’s $1 billion for Amtrak, the federal railroad that hasn’t turned a profit in 40 years; $2 billion for child-care subsidies; $50 million for that great engine of job creation, the National Endowment for the Arts; $400 million for global-warming research and another $2.4 billion for carbon-capture demonstration projects. There’s even $650 million on top of the billions already doled out to pay for digital TV conversion coupons. ~ A 40-Year Wish List: You won’t believe what’s in that stimulus bill, The Wall Street Journal, 28 January, 2009

RULE OF GOVERNMENT SACKS

It always seems as if the really dangerous power junkies are the ones that get sold to us with the most cutsie names.

The guy who used his Security Advisor ID to go into the National Archives and take Top Secret documents, shove them into his underwear and socks and later destroy them to protect one of the most corrupt administrations in history, he’s “Sandy”.2

The scumbag who viciously prosecuted two border patrol agents using convicted international drug pimps as witnesses to the point of ruining their lives and their families because they should have the temerity to do their jobs, he’s “Johnny”.3

And the shark who funneled billions of taxpayer dollars to his former firm while he was Treasury Secretary, he’s “Hank”.

In making his push to administer the largest federal bailout of Wall Street in history, Treasury Secretary Henry Paulson is seeking unfettered authority. McClatchy poses the question today, “can you trust a Wall Street veteran with a Wall Street bailout?,” referring to Paulson, the former CEO of Goldman Sachs:

But the conflicts are also visible. Paulson has surrounded himself with former Goldman executives as he tries to navigate the domino-like collapse of several parts of the global financial market. And others have gone off to lead companies that could be among those that receive a bailout.

In late July, Paulson tapped Ken Wilson, one of Goldman’s most senior executives, to join him as an adviser on what to about problems in the U.S. and global banking sector. Paulson’s former assistant secretary, Robert Steel, left in July to become head of Wachovia, the Charlotte-based bank that has hundreds of millions of troubled mortgage loans on its books.

Goldman Sachs cashed in under Paulson, with earnings in 2005 of $5.6 billion; Paulson made more than $38 million that year. A 2005 annual report shows that “Goldman was still a significant player” in issuing mortgage bonds. The conflict of interest is increasingly clear today, as Bloomberg reports that “Goldman Sachs Group Inc. and Morgan Stanley may be among the biggest beneficiaries” of Paulson’s bailout plan ~ Conflict Of Interest? Report Says Goldman Sachs ‘Among Biggest Beneficiaries’ Of Paulson’s Bailout, Satyam Khanna, ThinkProgress, 22 September, 2008

No firm defines “insider” better than Goldman Sachs whose alumni has so deluged the halls of political power that the investment bank has been renamed by observers as “Government Sachs”.

Goldman alums include:

* Former treasury secretary Hank Paulson

* Paulson’s bailout chief Neel Kashkari

* Interim Treasury investment officer Reuben Jeffrey

* Key Treasury players Dan Jester, Steve Shafran, Edward C. Forst, and Robert K. Steel

* Key New York Federal Reserve players Stephen Friedman (head of the New York Fed board of governors, who sat on Goldman’s board and owned a substantial stake in Goldman while he was making official decisions – and see this), William C. Dudley (head of the New York Fed’s unit that buys and sells government securities), and E. Gerald Corrigan (charged with convening a group to analyze risk on Wall Street) ~ Goldman Sachs Alumni Hold Many of the Top Government Positions, Alex Floum, The Examiner, 06 May, 2009

If Goldman thought they got a lucky break with George W. Bush, they must think they hit the jackpot with Barack Hussein Obama:

Goldman Sachs partner Gary Gensler4 is Obama’s Commodity Futures Trading Commission head. He was confirmed despite heated congressional grilling over his role, as Reuters described it, “as a high-level Treasury official in a 2000 law that exempted the $58 trillion credit default swap market from oversight. The financial instruments have been blamed for amplifying global financial turmoil.” Gensler said he was sorry…

Goldman Sachs kept White House Chief of Staff Rahm Emanuel on a $3,000 monthly retainer while he worked as Clinton’s chief fundraiser, as first reported by Washington Examiner columnist Tim Carney. The financial titans threw in another $50,000 to become the Clinton primary campaign’s top funder. Emanuel received nearly $80,000 in cash from Goldman Sachs during his four terms in Congress — investments that have reaped untold rewards, as Emanuel assumed a leading role championing the trillion-dollar TARP banking-bailout law.

Former Goldman Sachs lobbyist Mark Patterson serves under [Obama Treasury Secretary and former head of the NY Federal Reserve Bank Timothy] Geithner as his top deputy and overseer of TARP bailout — $10 billion of which went to Goldman Sachs.

Obama’s close hometown crony, campaign-finance chief and senior adviser Penny Pritzker, was head of Superior Bank of Chicago, a subprime specialist that went bust in 2001, leaving more than 1,400 people stripped of their savings after bank officials falsified profit reports. Pritzker’s lawyer at O’Melveny and Myers, Tom Donilon, is now Obama’s deputy national-security adviser. He earned just shy of $4 million representing her and other high-profile meltdown clients including Goldman Sachs.

White House National Economic Council head Larry Summers reaped nearly $2.8 million in speaking fees from many of the major financial institutions and government-bailout recipients he now polices, including JP Morgan Chase, Citigroup, Lehman Brothers, and Goldman Sachs. A single speech to Goldman Sachs in April 2008 brought in $135,000. Summers had prior experience negotiating government-sponsored bailouts that benefit private concerns. In 1995, he spearheaded a $40 billion bailout of the Mexican peso that bypassed Congress. Summers personally leaned on the International Monetary Fund to provide nearly $18 billion for the package. Summers’s boss, then–secretary of the Treasury Robert Rubin, was former co-chairman of Wall Street giant Goldman Sachs — the Mexican government’s investment banking firm of choice. ~ Obama and Goldman Sachs, Michelle Malkin, National Review Online, 21 April, 2010

Perhaps the first biggest myth is that the mega-corporations that make up “Wall Street”, rather than epitomizing “capitalism” actually have nothing to do with it.

Shortly behind it is the myth that the Democrat Party and Barack Obama are representatives of the “common man” in direct opposition to “the billionaires”.

Barack Obama may be the most owned presidential puppet in American history:

Employees from Goldman Sachs gave more to the Obama campaign than any other organization except the University of California — with Citigroup and JPMorgan Chase quickly following in sixth and seventh place. …

Risk-taking and speculation are good. But the Democrats’ crony capitalism is the worst of both worlds: risk-taking without any real risk for the risk-takers. It’s like gambling with your rich daddy’s money, except we’re the rich daddy. …

It took The New York Times a year and a half to figure out Goldman’s jackpot winnings from the AIG bailout — $12.9 billion, according to the Times… ~ Obama is Owned – You Can Bank On It, Ann Coulter, Townhall.com, 10 February, 2010

Behind the teleprompter, Obama blustered about how hard he was going to nail Goldman to the wall.

Behind closed doors, the only thing he was nailing was another round of Dom with Lloyd Blankfein, where they rehearsed what he would be saying next.

While Goldman Sachs’ lawyers negotiated with the Securities and Exchange Commission over potentially explosive civil fraud charges, Goldman’s chief executive visited the White House at least four times.

White House logs show that Chief Executive Lloyd Blankfein traveled to Washington for at least two events with President Barack Obama, whose 2008 presidential campaign received $994,795 in donations from Goldman’s employees and their relatives. He also met twice with Obama’s top economic adviser, Larry Summers. ~ Goldman’s White House Connections Raise Eyebrows, McClatchy, 21 April, 2010

When it came to who gets paid, the Mystery Marxist with a radical Left pedigree that would make Che Guevara jealous suddenly became Milton Friedman;

Barack Obama said he doesn’t “begrudge” the $17 million bonus awarded to JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon or the $9 million issued to Goldman Sachs Group Inc. CEO Lloyd Blankfein, noting that some athletes take home more pay.

…speaking in an interview, said in response to a question that while $17 million is “an extraordinary amount of money” for Main Street, “there are some baseball players who are making more than that and don’t get to the World Series either…”

“I know both those guys; they are very savvy businessmen,” Obama said in the interview yesterday in the Oval Office with Bloomberg BusinessWeek, which will appear on newsstands Friday. “I, like most of the American people, don’t begrudge people success or wealth. That is part of the free- market system.” ~ Obama Doesn’t ‘Begrudge’ Bonuses for Blankfein, Dimon, Julianna Goldman and Ian Katz, Bloomberg, 10 February, 2010

Oh I’ll bet you “know both those guys”, Barry … well. In spite of the dramatic hue and cry to start stringing Wall Street bankers up by their heels, Mr. Obama denied his base and covered for who butters his bread.

BRINING IT HOME

As the reality of this incestuous, perennial cesspool of money & politics finally begins to hit home, a silver bullet becomes forged in the furnace of citizen anger.

Suddenly an issue that crosses over old paradigms raises its head to Americans everywhere and starts to really piss them off: corruption.

“When you see the dollars the banks got, it’s hard to make the case these were successful institutions,” says Sherrod Brown, a Democrat Senator from Ohio who in 2010 introduced an unsuccessful bill to limit bank size. “This is an issue that can unite the Tea Party and Occupy Wall Street. There are lawmakers in both parties who would change their votes now.” ~ Secret Fed Loans Gave Banks $13 Billion Undisclosed to Congress, Bob Ivry, Bradley Keoun and Phil Kuntz, Bloomberg Markets Magazine, – 27 November, 2011

_____________________

- Throughout my walk as a Christian I have been frequently disturbed by how others, who call themselves “Christian” have so little respect for the Name of G-d. In the Time of Jesus Christ, Jews had such fear and reverence for the Name of G-d that they dared not speak it, instead calling Him only, “Ha Shem”, “The Name”. In fact, one of the most common Names of G-d, “YHWH” (known as “the Tetragrammaton”) is actually ineffable. There is no way to easily speak these 4 Hebrew consonants. Later, vowels were added for convenience but the names “Jehovah” and “Yahweh” are found nowhere in the Bible.

How often have you heard a Christian say the words “Oh my God!”? It is a vain (meaningless) usage of His Name and qualifies as blasphemy.

So, in an effort to draw the attention of Christians to this issue, I have taken the tradition of Orthodox Judaism which hyphenates the Name of G-d out of respect for that Name.

- For his high treason, suspended his security clearance for 3 years. He’ll never do that again!

- Lou Dobbs: Outrageous, Bush pardons 14 people, including drug dealers, but not Ramos & Compean, CNN Lou Dobbs Tonight | November 24, 2008 | Transcript

— Tonight an outrageous move from the White House, President Bush pardoning 14 people, including drug dealers. But not former border patrol agents Ramos and Compean.

DOBBS: President Bush today granted 14 pardons and he commuted two prison sentences. Five of those given clemency were convicted of serious drug charges. In what is an outrageous miscarriage of justice, former border patrols Ignacio Ramos and Jose Compean serving lengthy prison sentences were not included on the president’s list. They are serving those sentences for shooting and wounding an illegal alien drug dealer who they were pursuing and who was given immunity by the prosecutor to testify against those two border patrol agents. Hundreds of thousands of Americans have called for them to be released from prison. So far the White House has ignored those pleas and has done so again today.

- Gensler would later figure prominently when another Goldman alumni, former NJ Democrat senator and governor Jon Corzine ended up “losing” $1.2 billion in client funds. Losing a copule billion dollars of someone else’s money is just like when you lose your car keys, isn’t it? Hey! This guy should be in…wait, he is in government.

“I simply do not know where the money is,” Jon Corzine told Congress on Thursday. The man who led MF Global into bankruptcy claimed ignorance as to why more than $1.2 billion in client funds is still missing. But the former Democrat Senator and Governor did disclose some interesting details about his relationship with his primary regulator and former Goldman Sachs colleague, Gary Gensler.

Mr. Gensler, chairman of the Commodity Futures Trading Commission, repeated several times at a hearing last week that it had been 14 years since they had worked together at Goldman. ~ The Talented Mr. Gensler: Jon Corzine’s regulator wants you to know he’s been very busy, The Wall Street Journal, 12 December 2011